Keywords:

maker movement, indie designers, Italy, survey

By Massimo Menichinelli, Massimo Bianchini, Alessandra Carosi, Stefano Maffei

Introduction

The development and adoption of digital technologies in the past few decades has introduced new working conditions and modified some of the existing ones. New forms of organisation and new forms of distribution of resources have been enabled (or old forms have been modified or rendered obsolete) especially thanks to infrastructures such as the Internet (a global network of devices and technologies) and the World Wide Web (a global network of information and documents). Furthermore, there are also protocols and softwares that manage the interaction between both of these networks. Digital technologies have always been in part digital and immaterial with data and software, and physical and material with hardware and connections. This ecosystem has enabled the emerging of new forms of work, organisation, business and economic activity in many fields such as music, biotechnology, movies, science, art and so on, including design. Free Software, Open Source, Peer-to-Peer, Crowdsourcing, Sharing Economy, Diffuse, Distributed and Decentralised Systems are some of the many new definitions created in order to understand better the new phenomena of organisation of work emerged from the adoption of digital technologies, and especially the Internet and the World Wide Web. The concept of peer production emerged as a framework that aims at identifying the common traits in all these definitions regarding a new and relevant way of organising the work of distributed and autonomous individuals within the production and distribution of digital content characterised by collaborative practices, rather than competitive ones (Benkler, 2002).

This digital content, thanks also to the digitalisation of an increasing amount of types of information, encompasses many fields and disciplines, making peer production a promising means of organising knowledge work in future years. A new and relevant way for organising work on digital content, could also be restated as a new and relevant way for organising the design of digital content, understanding design both as “to plan and make decisions about (something that is being built or created)” or “to create the plans, drawings, etc., that show how (something) will be made”. Both are definitions of design according to the Merriam Webster dictionary (“Design”, 2015), and could refer to a general or broader (or even informal) activity of developing a content or project (i.e., like professionals who are not trained as designers or amateurs do) or to developing a project following the methods, culture, history, tools and roles of the Design discipline (i.e., designers). For example, software is digital content that can be “designed” (usually by people formally trained in software development, computer science and engineering, but increasingly by people with informal training); the design of websites is a specific form of software (and therefore digital content) that can be designed (usually by people formally trained in design, art, architecture, but increasingly by people with informal training).

Therefore, peer production can be applied to Design, but other phenomena in the past two decades have shown that it could be applied also to non-digital Design projects. As we have seen, digital technologies are both immaterial and material, physical and digital. Increasingly, the adoption of peer production is taking place not only in the context of the development of digital and immaterial content, but also during the design, manufacturing and distribution of physical goods. Furthermore, Open Design and Open Hardware projects are developed, discussed, manufactured and distributed thanks to digital fabrication and communication technologies, advanced funding initiatives (like crowdfunding platforms and hardware incubators) and globally integrated supply chains. This new systemic dimension of work is possible, among other factors, thanks to local facilities like Fab Labs, Makerspaces and Hackerspaces, where individuals can gather and form communities with other people, designing and manufacturing together. Such spaces represent the physical and geographically-located presence of the whole Maker movement, generally considered as a global community with collaborations taking place locally and globally at the same time. There are differences among these facilities, and the discussion about their definition is an ongoing effort: Within this paper we prefer to refer to them as Maker Laboratories, since the commonly used term “Makerspace” identifies only one part of the global community (Menichinelli, 2016), and the “Shared Machine Shops” term might not be always suitable to all of these labs, which in several cases have a limited set of machines and act more as a community place, especially in the Italian context that is the focus of this article (Menichinelli and Ranellucci, 2015).

Generally, the participants of this movement are referred to as Makers, and, while their existence is still an emerging phenomenon, it is widely acknowledged that they could exemplify a new and promising modality of work that reconnects people with traditions of manufacturing and craftsmanship, that enable more meaningful and empowering autonomous jobs and that joins creativity and social networks and impact (Anderson, 2012; Hatch, 2014). The dimension and impact of the Maker movement is a topic that is still understudied, but few studies showed that everyday citizens already innovate products by hacking them: Eric von Hippel and his collaborators found that in the UK, USA and Japan millions of citizens are engaging in consumer innovation activities related to products, and that their effort could be invaluable for the industry, especially in the UK, where such effort has been calculated to surpass the national companies’ R&D expenditures on consumer products (von Hippel et al., 2010; von Hippel et al., 2011). Such product hacking activities could be considered partially as related to a broad Maker movement, and they could also be improved by connecting such citizen innovators with existing Maker communities and Maker Laboratories that could foster such phenomenon and link it with industry. The physical dimension of digital technologies is now recognised as a promising dimension, and there is an increasing interest in developing products and services in this domain, rather than just digital services: Objects and manufacturing are increasingly digitalised (Anderson, 2010; Gershenfeld, 2005).

If Makers adopt, even if partially, peer production strategies, an analysis of their working and economic conditions could provide insights regarding the work dimension of the peer production of physical objects. This could expand the possibilities of peer production, which has been mostly tied to digital content so far. Furthermore, such analysis could give more insights on the sustainability of such practices and therefore be a starting point for suggesting policies for facilitating the sustainable development of such practices. This article addresses this issue by addressing the following related questions, but limiting the answers to the Italian context:

- What are the working conditions of Makers?

- How is peer production with physical goods taking place in the work of Makers?

- How are the working condition of Makers related to current social and economic trends?

In order to answer these questions, we adopted two approaches: a literature review (in order to understand existing approaches and the current social and economic situation) and an open online survey (in order to understand the emerging condition of Makers in Italy). We investigated the knowledge, values and working dimensions of Makers in Italy with the Makers’ Inquiry online survey. This research generated a first overview of the phenomenon in Italy (Bianchini et al., 2015), identifying the profiles of such Makers: An important step, because Makers are usually defined in a very broad way. Furthermore, we investigated their profiles regarding their values and motivations, in order to understand how much Makers engage in peer production or in traditional business practices, whether they work with open source and collaborative processes or individually, whether their communities have a strong role in their work or they are just a dimension with limited relevance. We then investigated their emerging business and working conditions: their market, expenses and commercial strategies, and the patterns regarding the ownership, access and use of manufacturing technologies. Finally, we compared these profiles with data regarding traditional designers and businesses and national context from existing literature.

Peer production and Makers: Physical things, physical places

The Internet and the World Wide Web have allowed the scaling up of projects in ways that were previously considered impossible, where complexity stops being a problem and could become a positive feature. With the emergence of Free Software and Open Source projects and, more specifically, with the Linux kernel project, practitioners and researchers have started to witness how the participation of a huge community in a project could represent a promising direction for the organisation of work. In the Linux kernel, for example, nearly 12,000 developers from more than 1,200 companies have contributed to the project since 2005 (Corbet et al., 2015). These principles and practices have spread also to different domains than software development, showing a promising strategy for organising design, work and management of complex projects (Goetz, 2003). Among the many new definitions created in order to understand better the new phenomena of organisation of work emerged thanks to the digital technologies, peer production has emerged as the explanation and generalisation of these processes. The term was coined by Yochai Benkler, who analysed many cases of collaborative design (intended with a broader definition) through the dimensions of organisation and management and proposed “peer production” (and especially, “commons-based peer production”) as a third way for organising work and business beside markets and managerial hierarchies (Benkler, 2002). Benkler generalised from the phenomenon of Free Software to suggest characteristics that make large-scale collaborations in many information production fields sustainable. Central to Benkler’s hypothesis is the claim that human knowledge, experiences and skills are highly variable and distributed: Peer production is important not as a technological innovation, but rather as an innovation on the organisation of work thanks to technology. In peer production, the distributed pool of users/designers participating in a project can better identify who is the best person for a task, with an improved identification and allocation of human creativity. As defined by Benkler, peer production is, therefore, an organisational innovation along three dimensions (Benkler, 2016):

- Decentralised conception and execution, based on the self-selection of the participants at work on a modular organisation of the project;

- Coexistence of diverse motivations (including non-monetary motivations) allows the participation of a large community of participants and

- The organisation is separated from property and contract, with inputs and outputs mostly governed as open commons (hence, the often-used term of “commons-based peer production”); the governance of resources and tasks are based on a combination of participatory, meritocratic and charismatic strategies rather than proprietary, contractual and hierarchical models.

According to Benkler, these characteristics define peer production against other definitions of mass-collaboration (or even mass-competition) phenomena: for example, in Crowdsourcing, the tasks are highly regimented and pre-specified by the project’s management, with the main goal of cost reduction, rather than distributed exploration of resources and possibilities. Peer production has, therefore, been considered a promising framework for understanding and managing large collective intelligence projects. The research on peer production, mostly developed in the field of social sciences and legal studies, has mainly focused on the topics of organisation, motivation and quality (Benkler et al., 2015).

As defined by Benkler and many other scholars, peer production is based on information for the self-organisation of participants and as the basis of the projects developed: the work is organised thanks to digital tools and data and consists of the collaborative development of modular projects of digital content. Thanks to ICTs, the costs for working (and distributing) digital content have lowered dramatically, making it easier to work on a large scale with digital content. There have been, however, many attempts at defining and experimenting how peer production could be applied to physical products beside only digital content. As noted by Clay Shirky, this could happen because: “An increasing number of physical products are becoming so data-centric that the physical aspects are simply executional steps at the end of a chain of digital manipulation” (Shirky, 2007). Early attempts at defining peer production for physical goods tried to understand a scenario of a society in which peer production is the primary mode of production, fulfilling the old Marxist postulate that control over the means of production should be in the hands of the producers, more specifically as commons (Siefkes, 2008). The most critical issues considered by Christian Siefkes were the coordination of production with consumption and the allocation of physical resources and goods (which, being rival goods, are limited, cannot be completely shared and are costly to distribute). Here, digital fabrication is already seen as a possible means of supporting these processes by allowing personal manufacturing as proposed by Neil Gershenfeld (2005) but not for completely solving all the issues of peer production for physical goods. Michel Bauwens also reflected on the possibilities for the peer production of physical things, proposing Open Design, Open Manufacturing, Open Money and P2P Energy Grids as its main strategies (Bauwens, 2009). In order to produce physical goods, there are inevitable costs of getting the capital together, and there needs at least to be cost recovery in order to make a project sustainable, therefore peer production as it emerged in digital content cannot be completely adopted. However, Bauwens suggested that the design process is the link between peer production and physical goods, since it is now largely an immaterial software-based process depending on the collaboration of several people. Therefore, a possible strategy could be the link between shared projects (Open Design) that can be prototyped and compiled in Maker Laboratories (Open Manufacturing) or with Open Hardware technologies like the RepRap 3D printer. Open Money and P2P Energy Grids are further elements that improve the sustainability of these issues on the financial and energetic dimensions.

Beside a few theoretical contributions about possible scenarios, a relevant amount of contribution has come from the practice of Open Design (Abel et al., 2011) and Open Hardware (Thompson, 2008) projects, where the first physical goods projects were designed and manufactured, facing many organisational, legal and business issues. Research on early Open Design projects (Raasch et al., 2009) showed it to be implemented in a substantial variety of projects with three different loci of production (external manufacturers, community or the focal organisation coordinating the project). In some cases that were examined, there is no clear-cut separation between design, prototyping and production in the community. Furthermore, it is important to point out that the researchers found some limitations to openness of the projects caused by the attempt to balance the interests of the designer community and commercial companies involved, like suppliers or manufacturers. Balka et al. (2009) found strong relationships between the stage of advancement of the development of Open Design projects and the size of the community, the presence of commercial contributors and the intensity of cooperation. However, the research reports that the number of people involved in the analysed communities mostly falls in the 2-10 range, with the range of 11-100 coming in second place, the range of only 1 participant in third place. The range of more than 100 participants is the last place, showing how peer production with physical goods was still limited to a few participants, compared to how its application to digital content was mostly considered relevant for the ability to scale to thousands of participants.

Open Design and Open Hardware are, therefore, the projects where peer production is applied to the design and manufacturing of physical goods, and their popularity, number of cases, dimension of communities and relevance have evolved considerably after these first analyses. It has been suggested that if Open Design and Open Hardware can be metaphorically compared to the “books” of commons-based peer production, then Maker laboratories are its libraries, that act as common points of access to stored knowledge and where new knowledge can be produced by providing general access to the tools, methods and experience of peer production (Troxler, 2011). Furthermore some of these spaces, especially Fab Labs, not only provide local access to digital and traditional manufacturing technologies, but also require the users to share their knowledge (CBA, 2012). Some research, however, has shown how the sharing of projects and documentation is still limited: an empirical study based on qualitative interviews with Fab Lab users found that the sharing of documentation and projects is limited by the difficulty of the task (especially when it involves tacit knowledge) and at the same time by the continuous evolution of the global Fab Lab community. Interestingly, these motivations are not the same for global online platforms, identified by researchers in previous literature (Wolf et al., 2014).

If Maker Laboratories are libraries for the peer production of physical goods, then the readers who come to these libraries are widely regarded to be the Makers. The term “Maker” has been generally referred to people who autonomously engage in the design and production of physical goods, from craft to electronics. Chris Anderson (Anderson, 2012) extends this definition stating that, furthermore, they use digital desktop tools to design and prototype new products; they follow cultural norms that prescribe to share and collaborate on those designs in online communities; they use common design standards that could enable the manufacturing of these projects by many actors and organisations beside the original designers or manufacturers. An empirical study of the development of the Maker identity shared by members of a small-town Hackerspace discovered that the identity of an established Maker is based on the development of a tool and material sensibility, on the adoption of an ad-hoci attitude and on the engagement with the broader Maker community (Toombs et al., 2014). Makers are generally considered a new kind of work that could generate new business and employment, with new dynamics, technologies and markets (Anderson, 2010, 2012; Hatch, 2014). The emergence of Makers is, however, still recent: the birth of the term is generally considered to be in 2005 with the launch of Make Magazine (Dougherty, 2005), and there is still a gap in the literature regarding the working conditions of being a Maker. The link between peer production and physical goods has been, therefore, established in practice thanks to Open Hardware and Open Design projects, developed and manufactured in Maker laboratories by Makers. The research on this topic is, however, still in its early steps, and while many contributions point to limits and differences in the peer production of physical goods, compared to digital content, more focus is needed on the organisation and the working conditions of such an approach.

Makers’ Inquiry: A national investigation about a new condition in Italy

The term “Maker” and the whole global ecosystem of Maker laboratories are recent phenomena and this aspect is even more relevant in Italy, where the first (temporary) Fab Lab was established in 2011, several years after many other countries had one (Menichinelli and Ranellucci, 2015). In order to explore the social, economic, cultural and technological dimensions of Makers in Italy, we set up the Makers’ Inquiry as an online survey developed during 2014. The Makers’ Inquiry was developed and coordinated by the Department of Design of Politecnico di Milano, in collaboration with the Make in Italy CBD Foundation and the Make in Italy Association; it was also supported by the DESIS Network.

The survey analysed Italian Makers in terms of which skills and capabilities they have, what kind of places they work in, which design processes and approaches they follow and what their social and economic statuses are, together with their working conditions. There are several different interpretations of the term “Maker”, and it is still difficult to know precisely how many Makers are in Italy and where they are (and, therefore, it is also difficult to reach them). For this reason, we decided to develop an open online survey in order to explore the emerging community of Italian Makers, rather than trying to precisely identify and quantify who they are. We provided three different meanings to the term Maker, from which participants could choose at the beginning of the survey:

- Makers as commonly understood and described in Make Magazine and other related authors (Anderson, 2012; Dougherty, 2005; The Blueprint, 2014): Makers as technologically advanced people who tend to use digital technologies for communicating, manufacturing and sharing their projects;

- Makers as Independent (Indie) Designers: Individual design actors that own or manage all the competencies related to design, production, and distribution processes, thus becoming self-producers (Bianchini and Maffei, 2012); and

- Managers of Maker Laboratories (since they both are probably a good example of Makers, and they work with Makers on an everyday basis).

We chose to reach potential Makers through online communities (the Facebook group Fabber in Italia), Maker laboratories and specific communications organised by the Make in Italy CBD Foundation and the Make in Italy Association. The survey was officially launched in July 2014 and closed at the end of October 2014: 214 participants partially completed the survey (which was composed by of questions divided into 11 sections, except for Maker Laboratories managers who were presented a further section dedicated to their work), and we chose to focus only on the participants who completed more than 50% of the questions, i.e., 134 participants. The online platform for the Makers’ Inquiry was developed with open source software (LimeSurvey Project Team and Schmitz, 2015) and the scripts specifically developed in order to manage information and elaborate data and graphs are also accessible online as open source software. In addition, the results of the survey have been released online as open data, accessible to the general public, the research community and the Maker community through a book (Bianchini et al., 2015), and at the 2015 Cumulus Conference (2015), in a paper investigating the Design education system evolution in the era of digital fabrication, which took into consideration the results of the Makers’ Inquiry (Menichinelli et al., 2015). The survey has focused only on the Italian context for the moment but there is the intention to spread the research to other countries worldwide thanks to the collaboration with other international institutions. In this way, the Makers’ Inquiry could allow the comparison of data from national Maker communities becoming a shared and collaborative tool for understanding the Maker movement. The online platform could also, at the same time, become a shared repository for research and data about Makers and Maker Laboratories.

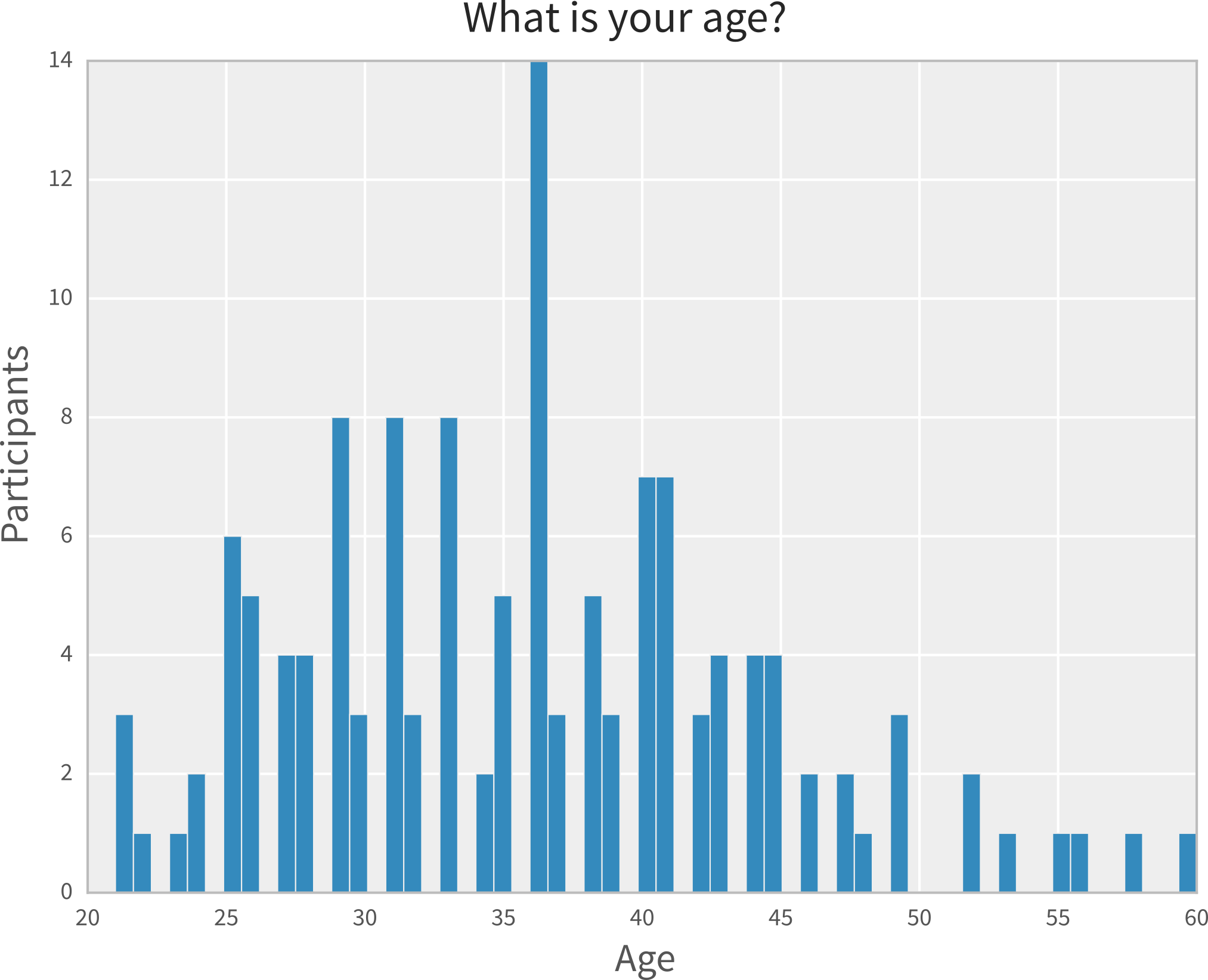

This article proposes a discussion from just a selection of questions composing the whole inquiry, in order to highlight the most important aspects regarding the connections among Makers, Maker Laboratories, peer production and work. We analysed the social, educational and economic dimension of Italian Makers, as a background for their working conditions and participation in peer production practices. First of all, the age of Makers ranges from 21 and 60 years old but the majority of them is between 30 and 40 years old, with a peak at 36 years (Fig. 1). The age of Italian Makers falls mainly in the range of the working age, showing how the identity of Makers could be linked to work. The majority of the participants lives with her/his partner (30.5%) and children (21.6%); less than 15% live alone or with her/his parents. Furthermore then, the Italian Maker scene is mostly composed by adults who have a family. Regarding their gender, 72.4% of them self-identifies as male, 23.4% as female and 3.7% prefers not to reply to the question.

Figure 1. The distribution of the age of the participants in the survey

Italian Makers are mostly highly educated and able to relate with international subjects: 88.8% of the participants speak English, 44.7% has a Master degree, 13.4% affirms to have a Bachelor degree and just 17.1% obtained only a high school diploma. The fields of specialisation of Italian Makers are mainly related to industrial design, architecture and engineering (i.e., mechanics, informatics and electronics); confirming, therefore, the identity of Italian Makers as based on the integration of both creative and technical skills related to project development.

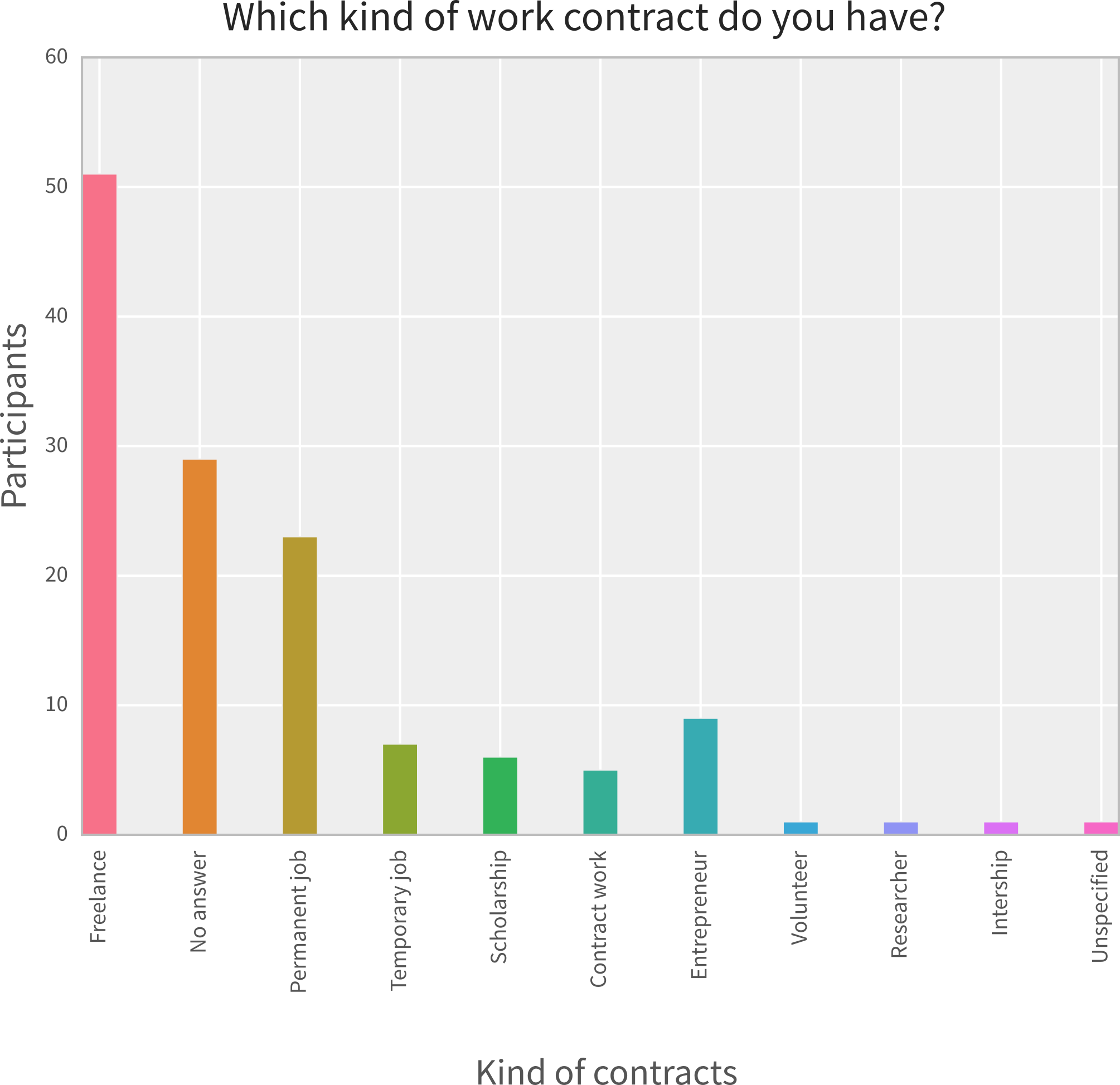

We then investigated the role of making in the economic and working conditions of participants: Making is mainly considered a secondary or complementary activity for the majority of the sample (54.4%). It is interesting to highlight that only 26.1% of the subjects consider it as a primary activity, while for 19.4% of the interviewed it is just a hobby. Therefore, making is not just an amateur activity for participants but it consists of a sort of serious profession in the principal working period of subjects’ life, even if only to a partial extent. In particular, as making is not considered the main activity of Italian makers, their principal occupation has been analysed. The majority of the sample (31.3%) declares to be mainly working as freelancers, while 10.3% are entrepreneurs and 19% are employed and just 6.7% are students. It can be stated that, in respect to the typology of work, the Italian Maker community is mainly composed by professionals who work in an independent and autonomous way, without being part of established companies (Fig. 2) Interestingly, 21.6% of them did not reply to the question (this is the most common value after being a freelancer), showing how working conditions might be unclear, a sensitive topic, or not fitting in conventional formats. It should be noted that within another survey about Maker Laboratories in Italy (Menichinelli and Ranellucci, 2015), a similar reaction was found around the topic of budget and business models for Maker Laboratories: here the reaction was even more extreme, with the majority of Maker Laboratories not answering about their budget and business models. The economic and work dimensions of Makers and Maker Laboratories in Italy is, therefore, either still emergent and underdeveloped, a critical and sensitive topic, or a dimension that Makers and Maker Laboratories are not aware of.

Figure 2. The work contract of the participants in the survey

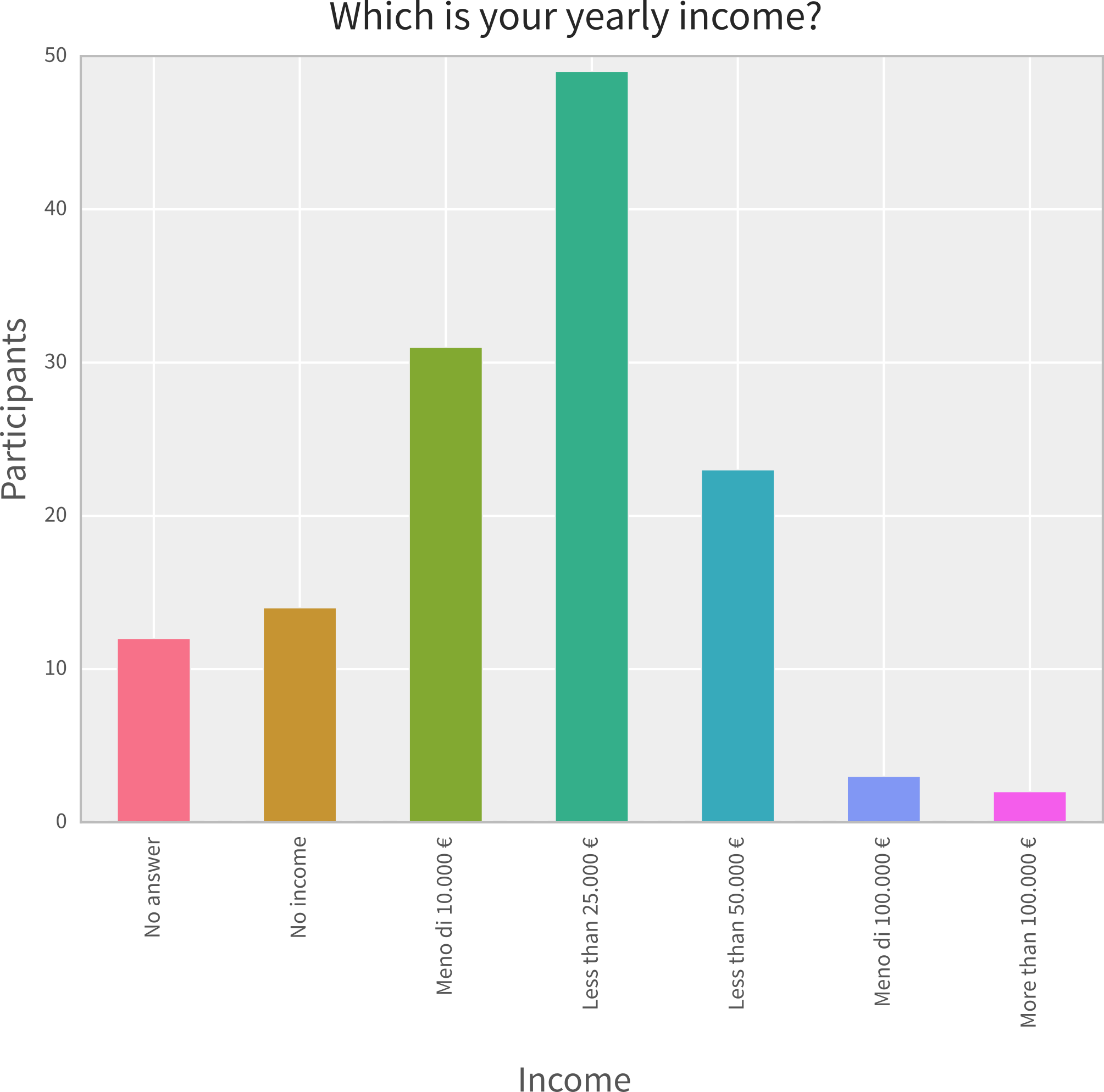

Referring more specifically to formal working conditions (eg, work contracts), a third of subjects (31.3%) works as freelancers (with or without VAT), while 17.1% have open-ended contracts and 5.2% fixed-term contracts, showing that making is mainly an independent and autonomous activity. Interestingly, 16.4% of the subjects mentioned other working conditions; however, when analysed in depth, they show that a further 7.4% of subjects have self-employed positions (9% are entrepreneurs then), bringing us to a 38.7% of subjects that are self-employed individuals. Therefore, even if making remains an emerging phenomenon, it can be considered as a new way of working professionally and not just a hobby. On one side, there are entrepreneurs and professionals of self-production and making, and, on the other, individuals who deal with making as a supplementary activity, maintaining another principal job. We also investigated the sustainability of the yearly income of Makers: the majority of participants (36.5%) earns between 10,000 and 25,000 €, while only 10.4% of the subjects have no income at all, and 23.1% earn between 0 and 10,000 €. On the higher end, 17.1% earn between 25,000 and 50,000 € (Fig. 3). The Italian average per capita income is 20,678 € (Cnel and Istat, 2014): The majority of Makers earns less or a bit more than the national average.

Figure 3. Yearly income of the participants in the survey

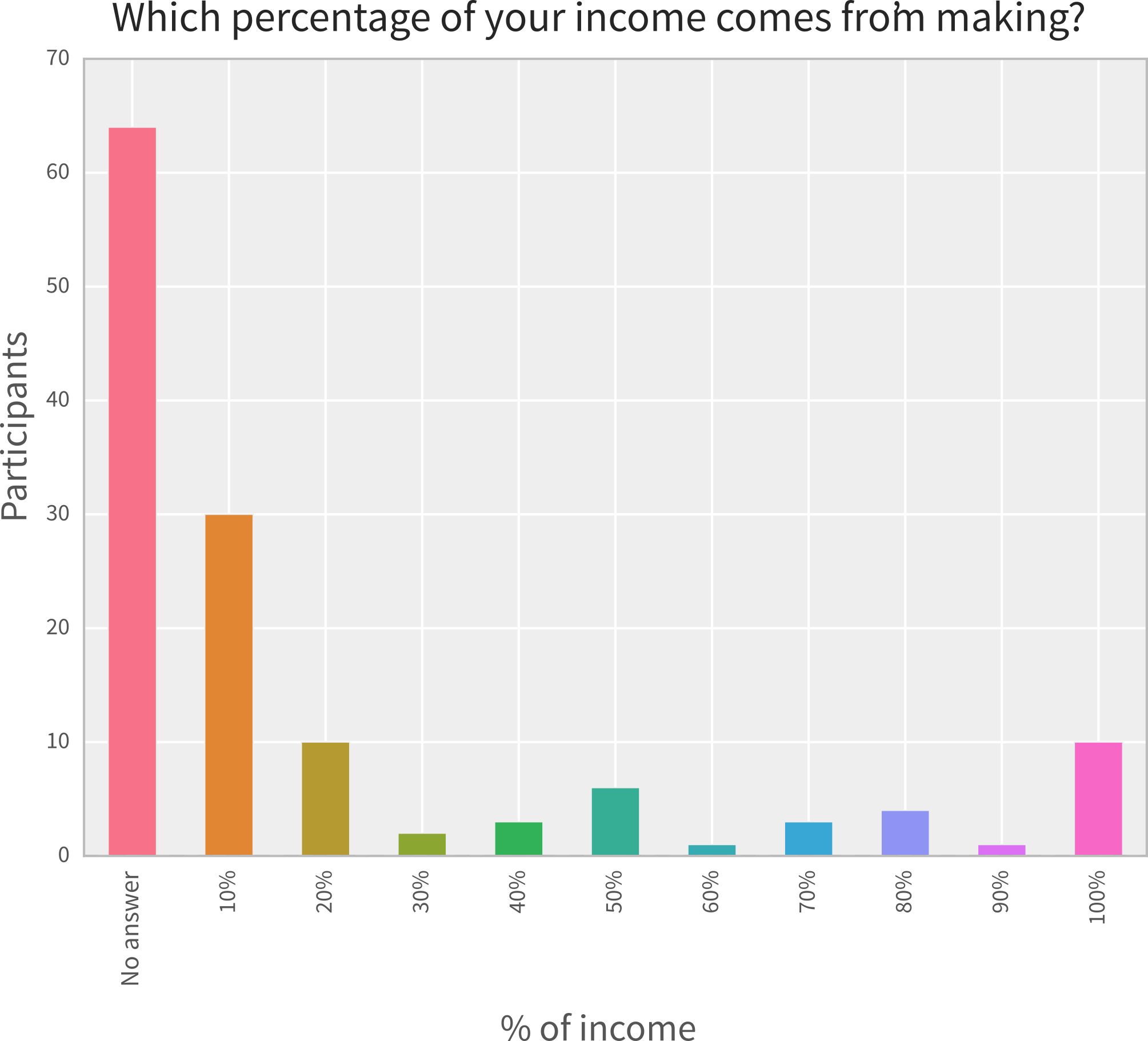

Furthermore, when it comes to defining the percentage of earnings directly deriving from making activities and self-production, a huge percentage of people did not answer (Fig. 4) showing how little impact making has on income or how Makers have a low awareness of such impact, or how sensitive this question could be. Among the ones who answered, making has been confirmed as a secondary activity: for 31.1% of the subjects, it contributes just in a minimum part of their salary (from 0% to 30% of the total income). A smaller group of people (9.5% of the sample) earns between 40% and 70% of their income from it, while just 11.4% of subjects obtain between 80% and 100% of their income from it.

Figure 4. Percentage of income coming from making for the participants in the survey

The activity of Italian Makers is mainly focused on producing prototypes (56.7%) and then manufacturing products in small batch runs (47.7%), personalised products (44%) and unique pieces (40.2%). Referring to quantities, 34.3% of the sample concentrates their work on 10 units/year, while 29% works on mini batch runs (18.6% until 50 units, and 10.4% until 100 units). Just 12.6% of subjects declared they produce more than 100 units per year. In relation to the target audience, Makers seem to sell a small amount of products to a wide audience of clients: professionals, private clients, distributors, traditional enterprises, and so on.

Their principal market (26.8%) consists of freelancers, traditional companies (20.1%), artisans (13.4%) and other Makers (13.4%). This data could suggest the existence of particular professional B2C channels, in addition to the classical B2B one. Furthermore, Italian Makers sell their products and services via B2C channels through distributors/traders (19.4%) and private clients (11.19%). There is a notable number of subjects who support Makers’ markets and encourage their activities; 23.1% are composed of friends and relatives, while 6.7% are investors (crowdfunding or venture capitalists). In conclusion, the great majority of Italian Makers mainly rely on their own resources through self-financing (71.6%) and, in a lower amount, through the resources they gain thanks to the sale of their products and services (46.2%). Just a small number of subjects rely on loans and credit (9.7%) or social financing like crowdfunding (8.2%). It can be stated at this stage Italian Makers are characterised by a traditional small business approach, investing enthusiasm and energy within an activity they like, and relying mainly on their personal and private resources.

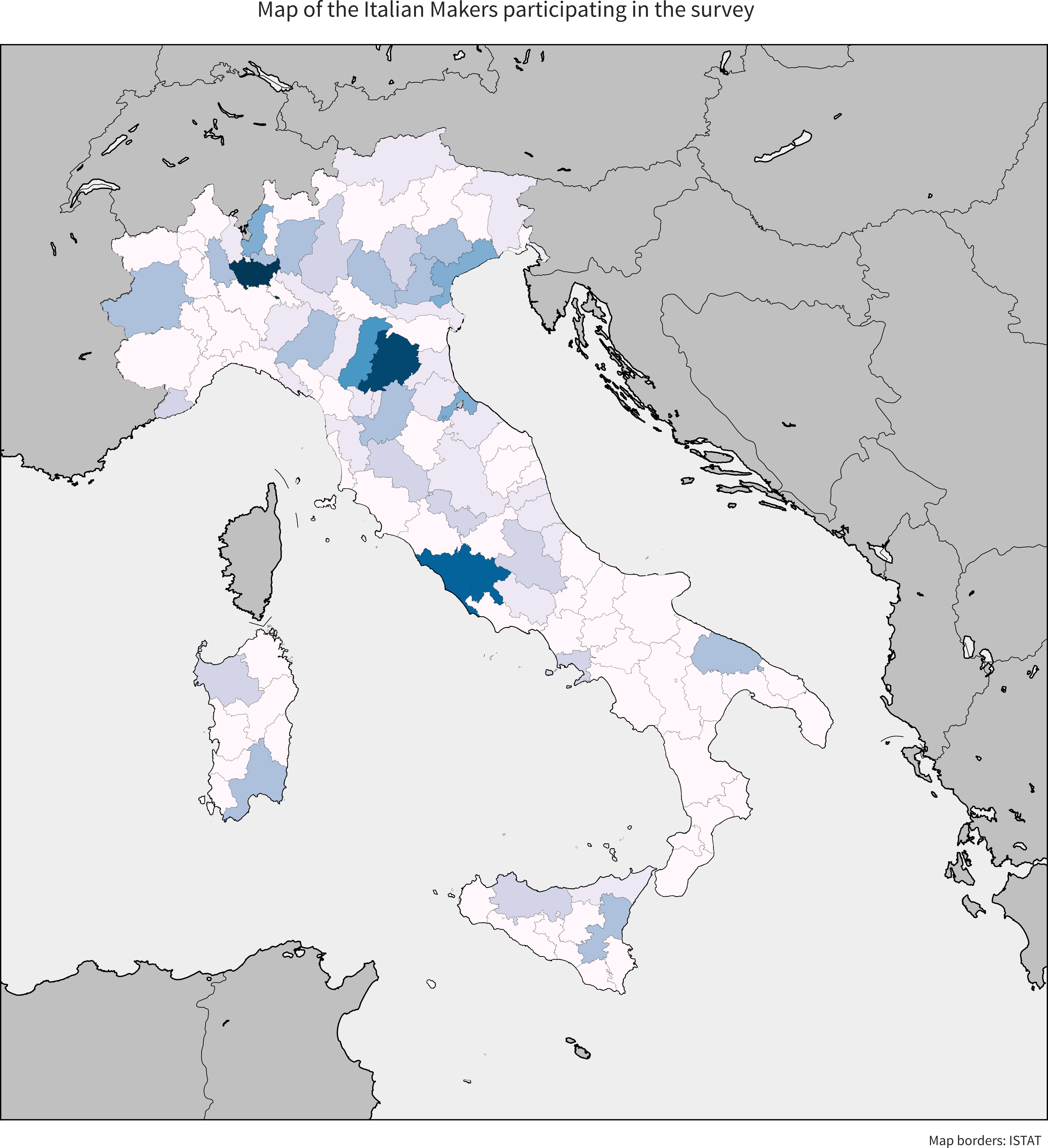

This data highlights a positive fact: Making activities are starting to provide some supplementary income for the people who undertake them. In some cases, such activities can become a professional opportunity for work: Making is evolving from a hobby activity to a professional job. One of the reasons for this condition could be addressed to the recent origin of this phenomenon in Italy, where making can be still considered a quite recent movement as a whole. Indeed, the majority of Italian Makers (60.4%) have only been involved in making activities for the past five years; 17.9% declares to have been involved making activities for less than a year, while 19.3% has practiced making for more than 5 years. The increasing interest towards making could be then linked to the global spread of the Maker Movement, but also with the Great Recession that took place in the years after 2007: Interest in making could be a consequence of the spreading of the “Maker meme”, but also as a consequence of the need to find new work opportunities in a period of crisis through self-employment. Furthermore, the phenomenon of the Maker in Italy has emerged more recently than in other countries, but it has found a prior “making knowledge” already embedded in historical Italian industrial districts. There is, in fact, an interesting overlap between the territorial concentrations of Italian Makers within historical industrial districts and urban contexts (Fig. 5): 27.5% of the participants lives in urban contexts (20,8% lives in Milan, Rome and Bologna as a whole) but 75 places have been mapped through the whole country. The higher concentration of Makers can be found in North and Central Italy, partially superimposed onto the pre-existing geography of industrial districts. Moreover, many Maker Laboratories and Italian manufacturers of digital fabrication technologies have a strong link with local productive systems. This means that there could be a partial continuity between traditional local production and the emergent working conditions of Makers.

Figure 5. Geographical distribution of the participants in the survey

We also investigated to what extent the working conditions of Makers in Italy can be related to peer production. We did not ask a specific question about peer production, but we asked several questions regarding many aspects of peer production: motivation for working, types of projects and approaches, values, participation in online and local communities in Maker Laboratories.

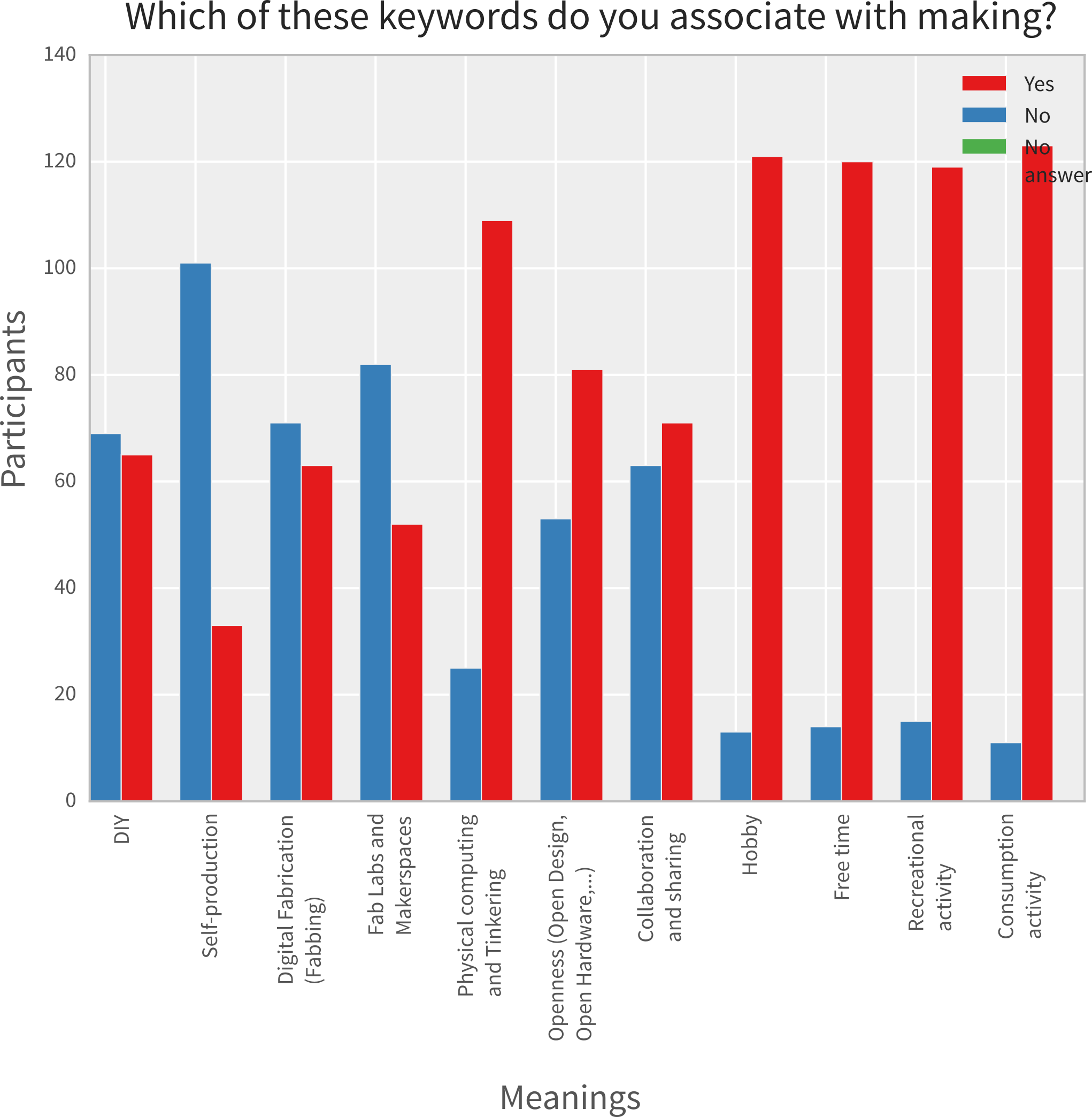

Regarding why people participate in making, the first motivation is the will to experiment (74.6%), followed by an interest in creating a product-service or launching an enterprise (64.9%), and then by an interest in learning (60.4%). However, social aspects like collaboration with other people is an important motivation only for 39.9% of subjects: a relevant percentage, but less than half of the participants are interested in collaboration. The idea of participation in making as an alternative for the capitalistic model of production and consumption of goods is accepted only by half of the participants (50.7%). In a similar way, a little bit less than half of the participants (44%) participate in making because of the possibility of generating a positive impact on their local community. In terms of keyword association, Italian Makers associate the term “making” with several different dimensions (Fig. 6). In first place, they relate it with self-production as an activity (75.3%), followed by Digital Fabrication as technology (52.9%), then with Maker Laboratories as places (61.1%) and DIY as an approach (51.4%). It is interesting to note also the association with the theme of Openness (Open Design, Open Hardware, Open Source Software) (39.5%) and with the Collaboration and Sharing condition (47.1%). Even if the majority of Makers do not associate making with openness, collaboration and sharing of knowledge and goods, a notable amount of participants do and their percentage is relevant. Therefore, it can be stated that collaboration and openness are still emerging ideas in making activities, not fully widespread, but already present and relevant.

Figure 6. Keywords associated with “making” by the participants in the survey

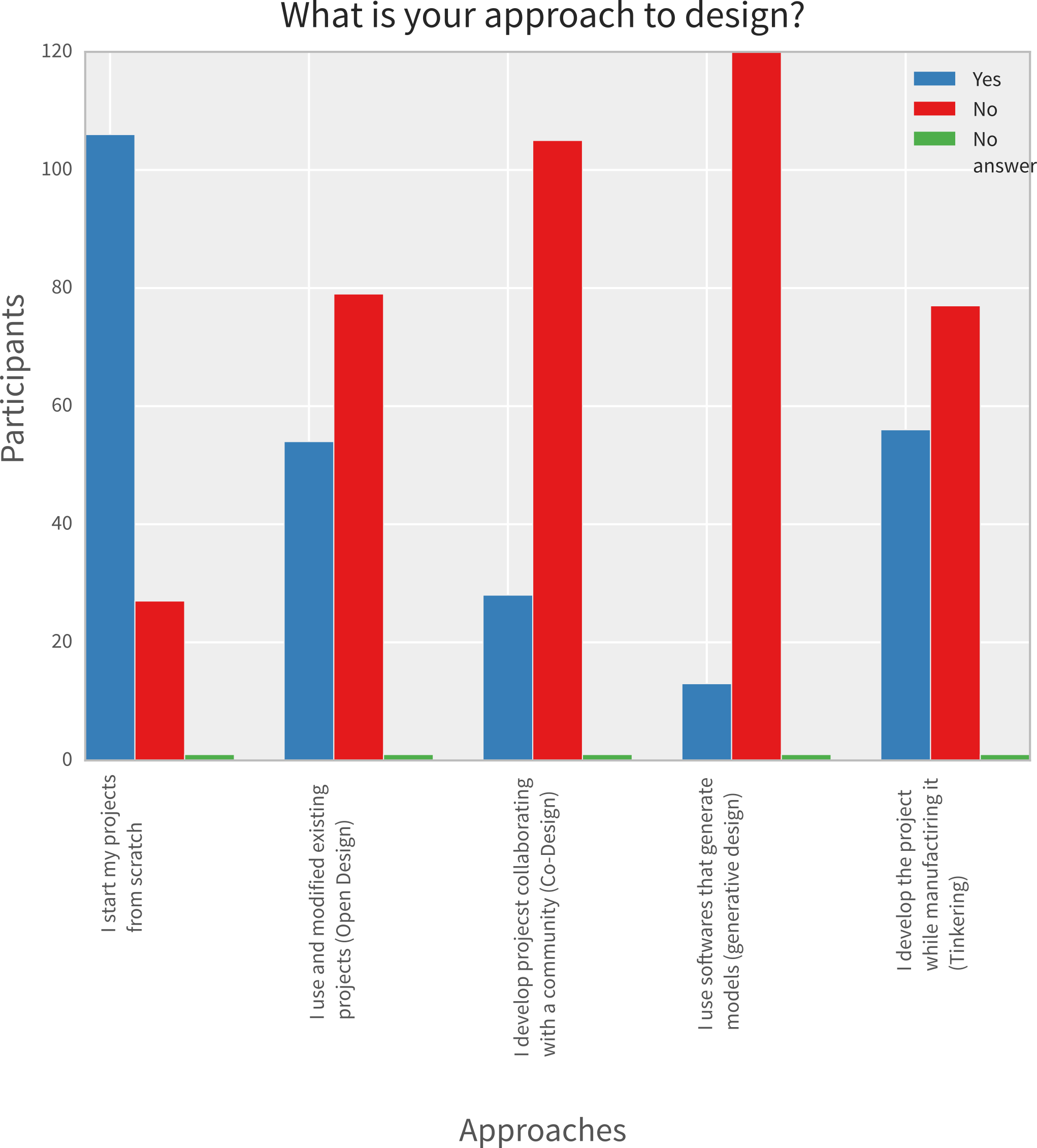

At the same time, even if sharing and collaboration are not clearly associated with making, the majority of the participants stated that they are more important than general information, technical knowledge, the organisation of initiatives, places for work and files and resources. Sharing and collaboration, therefore, are not considered to be originating from making, but are the most important traits. More insights about the approach to sharing and collaboration can be gathered from the question where we asked the Makers to choose an approach for their design processes (Fig. 7). While the majority of Makers prefer to start their projects from scratch (79.1%), Tinkering and Open Design follow at almost the same percentage (41.8% and 40.3%, respectively). Co-Design with a community then follows (20.9%) and Generative Design tools and approaches are the last option (9.7%). While Makers may still prefer to work individually, especially while experimenting with the materials at the same time of designing, the Open Design approach is highly relevant here.

Figure 7. Approaches to design processes by the participants in the survey

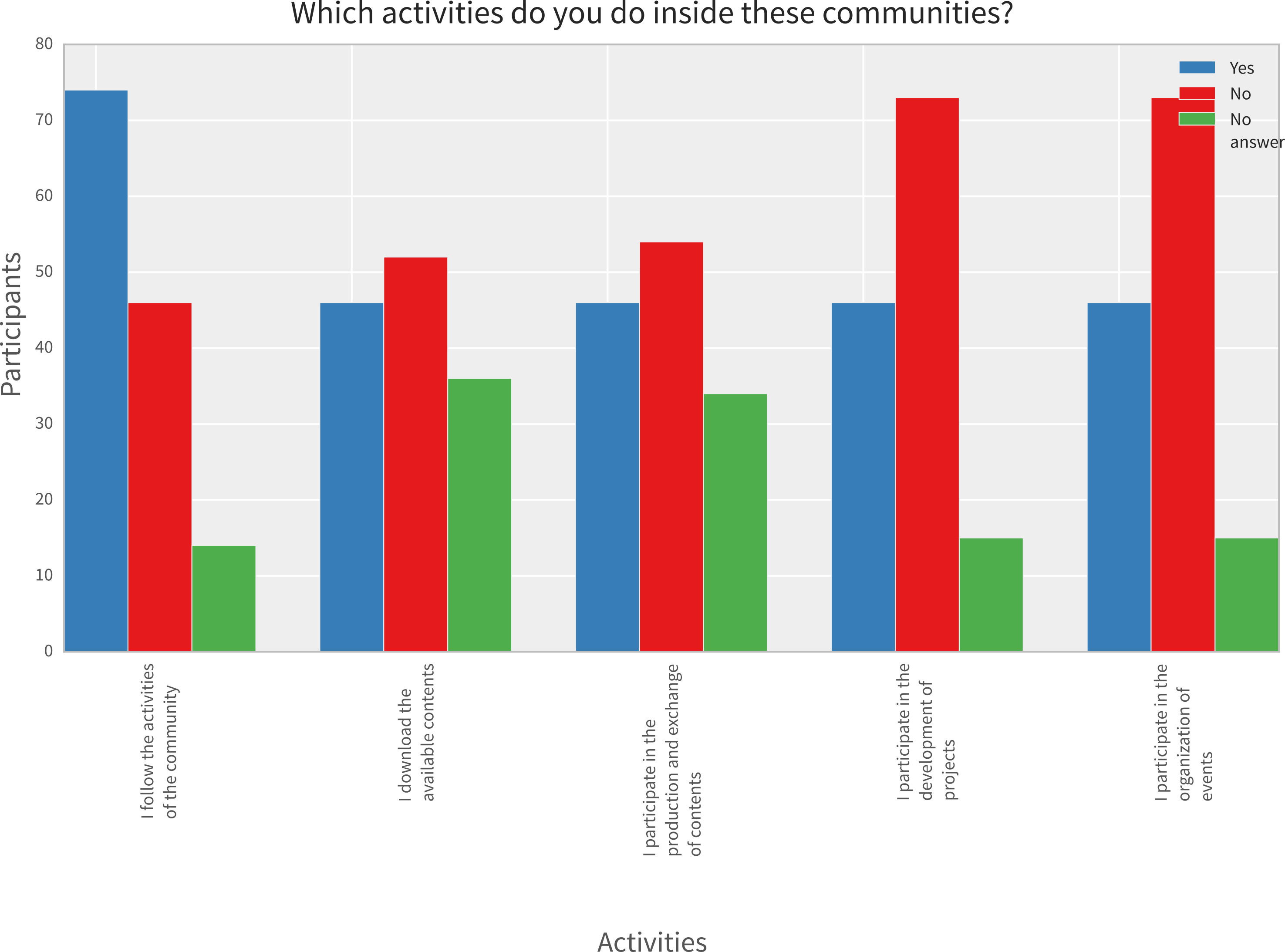

We then investigated to which extent Italian Makers participate in an online community or in local laboratories. The majority of them participates in an online community, specifying that they are members of the community (41.8 %) or that they participate while not being a real member (23.8%); 34.3% of them do not participate in an online community of Makers. The size of these online communities are mostly under 50 members (41.8%), but a relevant number of participants (26.8%) did not reply to the question, probably because they are not aware of the size of their community. The activities of these communities that the Makers participates in are also a good sign of the amount of collaboration and sharing (Fig. 8). Makers mostly follow activities passively (55.2%), but also download content (26.8%), and produce and share content (25.3%). While sharing and downloading content are activities with almost the same percentage (but with a higher proportion of unanswered questions compared to the other activities), active participation in working with other members takes place with a much less percentage: 11.2% for both the development of projects or events.

Figure 8. Activities in online communities by the participants in the survey

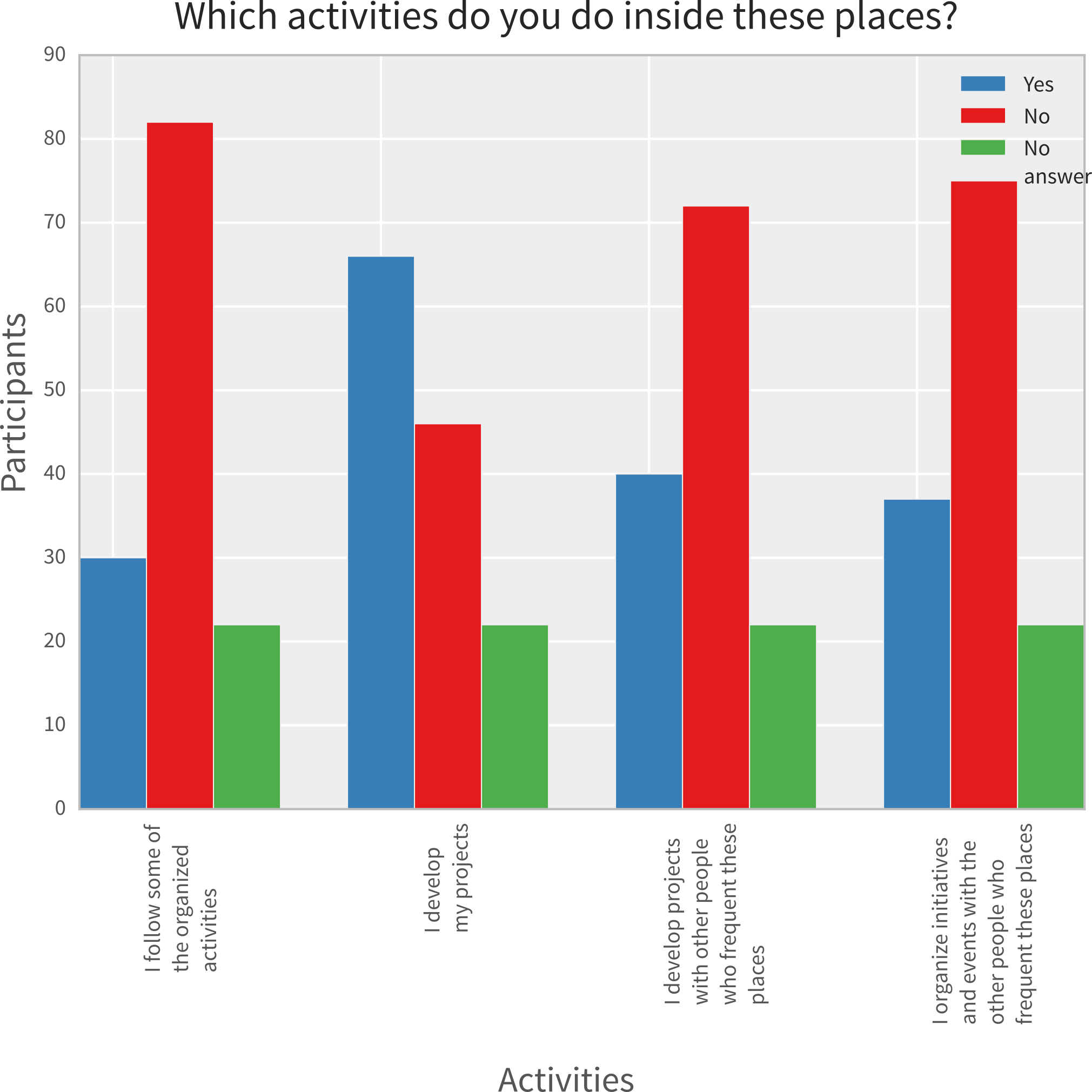

Regarding the participation in a local Maker Laboratory, 53.7% of the participants are active in one of them (even if with different levels of involvement), while 29.8% do not participate because they already own a private laboratory and 16.4% do not participate at all in a laboratory. These laboratories are mostly Fab Labs (35%), craftsmen’s workshops (18.6%) or Makerspaces (5.2%), among others. Here, again, we asked which kinds of activities the Makers were participating in, and generally the participation and collaboration was higher than in online communities (Fig. 9). Inside laboratories, Makers follow activities (22.4%), develop their projects (49.2%) or projects with others (29.8%) or initiatives and events (27.6%).

Figure 9. Activities in Maker Laboratories by the participants in the survey

Comparing the Makers’ Inquiry with other sources and the Italian context

There have been several investigations regarding peer production and projects related to making, but to our knowledge the Makers’ Inquiry represents the first attempt realised in Italy to explore the world of Makers in various dimensions beside the more common technological component. This section of the article aims at comparing Makers’ profiles and their work and economic conditions resulting from the Makers’ Inquiry with other research, statistics and literature. In our comparisons, we focused on three directions, comparing Makers with:

- The world of Design, with a specific focus on designers that self-produce their projects, (4.1);

- The world of Manufacturing that takes place outside Maker Laboratories but that adopts their technologies (4.2); and

- The general working conditions in Italy (4.3).

A preliminary consideration about the importance of analysing the Italian situation needs to be done: Within Western countries, Italy represents a notable context for observing the transformation taking place between the world of creativity and production. First of all, Italy finds itself in a leading position regarding the number of Fab Labs, and therefore it represents a relevant context for an analysis of Makers’ conditions (according to Fablabs.io, the official platform for Fab Labs, at the moment of writing—8 August 2016—Italy is the third country in the world for the number of Fab Labs). Secondly, Italy is one of the countries with the highest amount of micro-enterprises in Europe (Airaksinen et al., 2015), i.e., the organisation dimension coincides with the individual one (employed or freelance), and this fact represents an interesting point for the contextualisation of the system where Makers and Maker Laboratories are located.

Comparing Makers and designers

The first comparison can be conducted between the Maker and the figure of Indie Designers who follow the Designer=Enterprise or individual=organisation model (Bianchini and Maffei, 2012). Few official statistical data about designers’ working conditions in Italy (but also abroad) exist, and, in particular about Indie Designers. The latest information is dated 2013 (referring to data from 2012) and is contained within the Sector Study created by the Income Revenue Authority, which describes “Industrial and fashion design activity” (identified by the Cod. ATECO 74.10.10) and “Other design activity” (identified by the Cod. ATECO 74.10.90). The study investigates the fiscal position of 5,707 designers (product, fashion, interiors and graphic designers) referring to the year 2011, and it describes the typology and principal characteristics of the services they offered, their clients and markets, organisational forms and working places. The more interesting data concerns the category “Design studios selling self produced artefacts” (i.e., Indie Designers), whose presence is not substantial in terms of absolute numbers (representing 3.4% of the sample) but it certainly exceeds the number of large dimension design studios. Self-producers’ features can be highlighted as follows:

- They present a diversified clientèle composed of singular enterprises, private organisations and private subjects;

- 1/3 of designers realise 43% of their income with foreign clients, presenting a notable level of internationalisation;

- Their productive activities have a micro dimension: 61% of self-producers consists of individual enterprises relying on 1-2 workers; in just 20% of cases are there employees;

- 97% of designers are autonomous workers working independently; and

- Their prototyping/production space has a considerable importance. The overall working surface consists of 68m2, for 51% of the sample 48m2 are set up as laboratory for prototyping and production.

In 2012, before the Makers’ Inquiry, a non-scientific analysis called Designers’ Inquiry was developed in order to investigate the working conditions of designers, focusing particularly on their precarious conditions (Cantiere per pratiche non-affermative, 2013). Conducted on a sample of 767 designers aged between 21 and 35 years old (96% of them were Italian), the survey highlighted some particular aspects on their economic condition: Younger designers have very few earning with irregular incomes (32% affirms to gain from 0 to 5,000 € per year and 40% between 5,000 and 20,000 €), 33% of them needs to have a second complementary job in order to integrate their income, there is a lack of tutelage for designers and, in general, there is a need to develop a network of contacts in order to obtain some collaborations.

Some common findings between the results of the Makers’ Inquiry and the Designers’ Inquiry include:

- The relationship with a diversified market composed by both B2B and B2C channels;

- A working and contractual condition based on self-entrepreneurial activity;

- The need to develop integrative earnings (design or making can be considered both the first or second activity together with something else);

- The direct link between the working condition and the presence of places (private or public) accessible for prototyping artefacts or experimenting with technologies;

- The interest in having other places (like Maker Laboratories) able to integrate personal workshops or private production space;

- An activity strongly focused on the development of a network of personal relationships and contacts in order to start generating commissions and support business activities;

- A strong continuity and proximity between personal and professional life;

- The importance of familiar and friend networks in supporting the creation and development of their market; and

- An activity developed thanks to strong personal motivation enabling them to also face unfavourable working conditions.

It should be noted, however, that the Designers’ Inquiry does not mention peer production and the importance of collaborative communities, while competition and the competitiveness of designers is well described.

Comparing Makers and manufacturing enterprises

It is also important to compare Makers and traditional or established manufacturing enterprises, especially considering their reciprocal integration. This topic is still under-studied, but we have found an interesting source in the first report on digital technology impact on the Italian manufacturing system, created by Fondazione Nord Est and Prometeia for the Make in Italy CDB Foundation using a sample of 1,000 Italian firms. This report describes the “Make in Italy” as a transformation of the “Made in Italy” through the spread of the Makers movement under the influence of digital fabrication technologies (Fondazione Nord Est and Prometeia, 2015). The report depicts Makers in Italy as “a still very fragmented world, with the potential to erupt, with great innovative capabilities and high possibilities of transferring its innovations to more structured enterprises” (p. 11, English translation of the authors of this article). The study suggests that digital fabrication technologies and Makers can foster innovation and the valorisation of human capital by developing advanced technology profiles, by introducing innovative elements in traditional enterprises and by reinforcing the competitive capabilities of the entrepreneurial system. The report mentions Makers only in the introduction, mainly referring to the theme of digital craftsmanship, i.e., the forms of manufacturing production characterised by the use of digital technologies. There is no specific reference to the working condition of Makers or to peer production. Therefore, some of the themes at the basis of the Maker culture have not been faced in this analysis of digital technologies influence within tradition manufacturing enterprises.

An important section of the report describes the adoption of digital fabrication technologies, also focusing on the factors preventing or slowing the technology diffusion, such as 3D printing. It is interesting to highlight how finding professionally-trained workers able to develop the use of these technologies (as Makers could be) is not perceived as an important problem for the firms. A further confirmation of the actual distance between Makers (and their values) and enterprises can be noticed in another section of the report that describes the actors the enterprises deal with in order to obtain information and updates on digital technology development. Also, in this case, Makers as individuals or communities of professionals and workers are not even contemplated. The theme of the Maker community is represented regarding the relationship between manufacturing enterprises and Maker Laboratories, which, however, turns out to be very weak at all levels: Makers and Maker Laboratories are considered the less relevant actors when it comes to talk about technology. This fact could be interpreted in different ways, first of all, the recent development of the Maker movement and the scarce number of Maker Laboratories compared to firms. The final section of the report has a specific focus on the role of Maker Laboratories and defines two different development strategies: on one side, such laboratories could become stable partners for enterprises; on the other side, these laboratories could work on education and on the spreading of digital manufacturing within enterprises and the civil sector. In the first category, professional Makers operating as collaborators/business partners would prevail, while, in the second one, Makers operating as volunteers would prevail.

In conclusion, it can be highlighted that many common areas and similarities between the working conditions of Makers and designers emerge, while the integration between Maker Laboratories and enterprises still remains very limited. In particular, comparing the Makers’ Inquiry and the report realised by Fondazione Nord Est and Prometeia (Fondazione Nord Est and Prometeia, 2015), the following notable elements can be considered:

- The partners of manufacturing enterprises are not Makers meant as individual workers/professionals, but Maker Laboratories meant as organisations containing those communities;

- Within the industrial context, Makers do not seem to be considered yet as professional profiles by enterprises for the development and the use of digital technologies; and

- The relationship between manufacturing enterprises and peer production, ideally represented by Maker Laboratories, presents a residual and scarce value. The relationship between communities of professional Makers and enterprises do not take into consideration peer production: Instead, it focuses on consulting services, while the peer-to-peer dimension seems to be more connected with the field of education/learning where voluntary work prevails.

Contextualising Makers within current Italian working conditions

The relationship between working conditions as emerging from the Makers’ Inquiry can be briefly contextualised with national working conditions. In this section, we therefore compare it with the working conditions for freelance workers, for enterprises and for cooperatives.

As a starting point, we considered the national statistics, as collected and elaborated by the national institute for statistics, ISTAT (ISTAT, 2015) (see Table 1). Relevant issues can be found: inactive persons during working age (23.4%) are more than self-employed persons (9.1%) and almost as much as employed people (27.8%). Even with such a small percentage of self-employed workers, Italy is the second country in Europe for the proportion of self-employed persons over employed persons (Teichgraber, 2016). Meanwhile, unemployment has risen to 12.7%, and 15-24-year-old young persons face a 42.7% unemployment rate. Employment is more prevalent in Northern Italy (64.3%) than Southern Italy (41.8%).

Table 1. Working conditions of the national resident population in Italy (ISTAT, 2015)

|

No. |

Working conditions |

Absolute values |

% |

|

1 |

Working persons |

22,278,917 |

36.9 |

|

2 |

Self-employed |

5,498,719 |

9.1 |

|

3 |

Full-time |

4,661,964 |

7.7 |

|

4 |

Part-time |

836,755 |

1.4 |

|

5 |

Employed |

16,780,199 |

27.8 |

|

6 |

Full-time with an open-ended contract |

11,921,652 |

19.7 |

|

7 |

Part-time with an open-ended contract |

2,581,226 |

4.3 |

|

8 |

Full-time with a fixed-term contract |

1,604,319 |

2.7 |

|

9 |

Part-time with a fixed-term contract |

673,002 |

1.1 |

|

10 |

Persons looking for a job |

3,236,007 |

5.4 |

|

11 |

Inactive persons of working age (15-64 years old) |

14,121,771 |

23.4 |

|

12 |

Not actively looking for a job but available for working |

1,868,949 |

3.1 |

|

13 |

Not looking for a job but available for working |

1,504,670 |

2.5 |

|

14 |

Actively looking for a job but not available for working |

277,320 |

0.5 |

|

15 |

Not looking for a job and not available for working |

10,470,832 |

17.3 |

|

16 |

Inactive persons not of working age |

20,811,214 |

34.4 |

|

17 |

<15 years old |

8,438,807 |

14.0 |

|

18 |

>64 years old |

12,372,407 |

20.5 |

|

19 |

National resident population |

60,447,909 |

100.0 |

The current situation of the Italian community of Makers observed through the Makers’ Inquiry has shown a variety of professional figures among its members. Many of these subjects are connected with professional orders and associations, social cooperatives, cultural associations, social centres, research and innovation institutions. All these organisations are formally or informally a place for professional representation, and they all are now facing the overall transformation of work into more flexible and independent forms. This issue is directly linked to the recognition of making and Makers as a working condition and a specific profession. To date, Italian Makers are facilitated and up to point represented by associations (Make in Italy, Social Fab Lab) and Foundations (Make in Italy CDB), though they still lack a formal legal status. For example, statistical codes identifying the economic activities (e.g., NACE codes) do not report official descriptions regarding making-related activities, as expressed by the Maker movement. Economic activities, such as prototyping and self-production, which are common among Makers, are attributed to design, architecture and engineering professions. In Italy, self-production is considered an economic activity in the field of design (Ateco code 74.10.1 – Industrial Design and Fashion activities), while prototyping is classified as activity developed by technical draughtsmen and designers (Ateco code 74.10.3).

Italian Makers seem to be prevalently self-employed or entrepreneurs (38.7%), which is several times the 9.1% national level of self-employment; furthermore, self-employed workers are 24.6% of the working population, still a lower number than the ones emerging from the Makers’ Inquiry. A third of the Italian Maker Laboratories are characterised by the presence of co-working in their facilities (Menichinelli and Ranellucci, 2015), showing further the connection between self-employed workers and the Maker movement. Another emerging bond in this direction connects Maker Laboratories and professional associations. The growing geographical distribution of Maker Laboratories facilitates the connection with local chapters of professional associations (architects and engineers) by becoming accredited training centres for the professional development of architects and engineers. The phenomenon of self-employment in Italy is connected to the issue of precarious work, especially in the creative industries (Arvidsson et al., 2010) but also by the development of mixed forms of passionate work (McRobbie, 2015, 2016) and total work (Busacca, 2015) characterised by continuous learning, autonomy, responsibility, flexibility, individualisation, depreciation and cooperation. Within this context, Making activities are seen in Italy as an opportunity for new jobs or for the regeneration of existing skills in current jobs. However, the condition of self-employed workers in Italy is increasingly deteriorating: Between 2008 and 2013, 400,000 self-employed workers stopped working (7.2% of all self-employed workers) (Balduzzi, 2015; Huffington Post, 2013). This has led some journalists to elaborate that self-employed workers are nowadays the new proletariat in Italy, or at least the new working poor (Quinto Stato, 2014).

There is generally very little data about the integration of Italian Makers with firms, but we can focus on their contract and working condition in order to start exploring this topic. Regarding employed workers in firms, 22.3% of the subjects of the Makers’ Inquiry work in this condition (17.1% has an open-ended contract and 5.2% has a fixed-term contract), which is similar to but lower than the national data (27.8% employed, 24% with an open-ended contract and 3.8% with a fixed term contract); only for fixed-term contracts do subjects of the Maker’s Inquiry have a higher percentage (hinting again at the precarious and emerging nature of making activities). However, we should also note that since 2008 the number of firms in Italy has been in decline down to 4,390,000 units with 16,427,000 employees. Furthermore, the percentage of firms capable of surviving one year after establishment is also a critical factor (76.1% of firms born in 2012 were still active in 2013); regarding making, it should also be noted that 77% of Italian firms work in the service sector, which comprises almost 66% of all the employees (ISTAT, 2015), showing the current limitations of manufacturing in Italy. A very important feature of the Italian economic system is the prevalence of micro firms (0-9 employees), representing, in 2012, 95.2% of all active firms and 47.5% of all employees, creating an added value of 30.8%. Instead, large firms (with 250 or more employees) represent 0.1% of Italian firms and 19.4% of Italian employees for 31.5% of added value generated.

Given the fact that Makers are generally interested in collaboration and sharing, we could expect a relevant role of cooperatives in this movement as well. However, we find this aspect limited, in line with national data. For example, among the 70 Maker Laboratories that were analysed in Italy (Menichinelli and Ranellucci, 2015), only 4.3% were born out of the initiative of a cooperative, and only 2.9% are cooperatives. The status of Italian Maker Laboratories is instead much more linked to informal organisations (23.2%) or not recognised (i.e., an entity with no legal personality; 11.6%) or registered (36.2%) associations. In Italy, there are 301,191 non-profit organisations employing 951,580 paid employees (71.5% open-ended contracts, 28.4% fixed-term contracts) and 4.7 million volunteers. Almost 2/3 of such organisations are not recognised associations (who employ 12.4% of workers and 62.4% of volunteers). Social cooperatives represent 3.7% of such organisations but employ the majority of workers (47.1%) and the least amount of volunteers (0.9%) (ISTAT, 2015).

At the present time, the “Make in Italy” system that comprises Makers, Maker Laboratories, enterprises and organisations seems more focused on structuring its community thanks to the aggregative role played by local laboratories (connecting individuals), rather than using local Makers’ alliances to generate economic activities based on new forms of cooperative works. Italian Makers are mainly self-employed and not officially recognised workers, participating in local laboratories that are mostly informal organisations or non-profit associations. This condition could be seen as a limit to the development of making as an officially recognised economic activity or, on the contrary, as the embryo of a new way of working linked to an informal economy.

Conclusions

We investigated the knowledge, values and working dimensions of Makers in Italy with the Makers’ Inquiry, a survey that focused on Makers as represented by Make Magazine, Independent Designers and managers of Maker Laboratories. This research generated a first overview of the phenomenon in Italy, identifying the profiles of such Makers; this is an important step because Makers are usually defined in a very broad way. Furthermore, we investigated their profiles regarding their values and motivations, in order to understand how much Makers engage in peer production or in traditional businesses, whether they work with open source and collaborative processes or individually, whether their communities have a strong role in their work or they are just a dimension with limited relevance. We then investigated their emerging business and working conditions. Finally, we compared the gathered data with data regarding traditional designers, businesses and the national context. Given the recent nature of the Maker movement, the focus of this article is on providing a first overview of the phenomenon in Italy with an exploratory analysis and with comparison with existing related literature or national data, rather than contextualising the Maker movement in sociological and political terms. Such contextualisations could be a further step for future research.

Far from happening in a void and being a completely unexpected revolution, Italian Makers have a strong relationship with their localities and established industry. The majority of Italian Makers has been involved in making activities for the past five years; therefore, this is a recent evolution, where Makers work with a broader palette of projects and strategies: with both non-commercial and commercial activities, and both peer production and traditional approaches. The activity of making is still a secondary working activity that partially covers the Makers’ income, who are mostly self-employed working at home, in a craft workshop or in a Fab Lab in self-funded or non-commercial initiatives, where technology is not the only critical issue. After analysing the data from the Makers’ Inquiry, we can affirm that Italian Makers have an interest towards collaboration and peer production and, in particular, that the will to collaborate mostly derives from the necessity of technological skills and capabilities acquisition but it is also an issue that is informally considered important. A notable interest towards openness is also present but we could not find any useful information that could have helped us in differentiating the Maker approach to openness when it comes to digital (i.e., open software) and physical (i.e., open hardware) content. Italian Makers associate making with openness but not as its main trait, but their practice has a stronger relationship with openness than what Makers are aware of. Participation in communities is relevant, but there is more collaboration in Maker Laboratories than in online communities. Italian Makers do practice Open Design, but the gathered data suggests that peer production for physical goods in the context of Makers is still limited (in approach and scale of production), at an early stage, more linked to practice than ideology. As found in the existing literature about peer production with physical goods, there is a need for more practice and research in order to close the gap with peer production of digital content. The working conditions of Italian Makers is emergent and still not completely economically sustainable, but more similar to a job than to a hobby. Even if only a part of their income comes from making and making is mostly a secondary activity (and there is no official legal status for Makers in Italy), they are more interested in making as a job than as a hobby and their age falls in the working-age range.

The data gathered shows some interesting information that, however could be applicable only to an Italian context. Nevertheless, the survey could be a starting point to compare the same phenomenon in different countries. Therefore, on makersinquiry.org we released the survey files, software and data as open source in order to facilitate the adoption, modification, verification and replication of the survey. The replication of such a survey in more countries could both lead to an improvement to the survey, tools and approach and a further example of peer production, in the context of Design research. The connections among Makers, Maker Laboratories, peer production and work are growing, but further research is needed on the topics of peer production with physical goods and on the topic of policies that could improve the working condition of Makers in order to be more sustainable. Some contributions suggested that consumer innovation already plays a huge role in society, and we think that the Maker movement could be integrated with such phenomenon, as both are based on product hacking by everyday citizens. If this integration takes place and has a relevant dimension, it would therefore be important to understand how to make making activities more sustainable. We suggest that future research should gather more data and compare the available data with theoretical contributions about working conditions of especially self-employed workers and non-profit organisations, with the aim of elaborating policies that recognise and support the Maker movement and its impact on society and economy. Furthermore, we suggest to adopt alternative approaches for studying this topic, extending this research from a survey to other perspectives, since one approach alone cannot understand the complexity of the phenomena.

References

Abel, B., L. Evers, R. Klaassen and P. Troxler (eds.) (2011) Open Design Now: Why design cannot remain exclusive. Amsterdam: BIS Publishers. Available at: http://opendesignnow.org/.

Airaksinen, A., H. Luomaranta, P. Alajääskö and A. Roodhuijzen (2015) “Dependent and independent SMEs and large enterprises”. Available at: http://ec.europa.eu/eurostat/statistics-explained/index.php/Statistics_on_small_and_medium-sized_enterprises (accessed on 31 December 2015).

Anderson, C. (2010) “In the Next Industrial Revolution, Atoms are the New Bits”. Wired 18(2). Retrieved from http://www.wired.com/magazine/2010/01/ff_newrevolution

——— (2012) Makers: The New Industrial Revolution. New York: Crown Business.

Arvidsson, A., G. Malossi and S. Naro (2010) “Passionate work? Labour conditions in the Milan fashion industry”. Journal for Cultural Research 14(3): 295–309.

Balduzzi, G. (2015) “Non siamo più il Paese delle partite Iva”. Available at: http://www.linkiesta.it/it/article/2015/12/23/non-siamo-piu-il-paese-delle-partite-iva/28691/.

Balka, K., C. Raasch and C. Herstatt (2009) “Open source enters the world of atoms: A statistical analysis of open design”. First Monday 14(11). Available at: http://firstmonday.org/htbin/cgiwrap/bin/ojs/index.php/fm/article/view/2670/2366.

Bauwens, M. (2009) “The Emergence of Open Design and Open Manufacturing”. We_magazine 2. Available at: http://www.we-magazine.net/we-volume-02/.

Benkler, Y. (2002) “Coase’s Penguin, or, Linux and The Nature of the Firm”. The Yale Law Journal 112. Available at: http://www.yalelawjournal.org/the-yale-law-journal/content-pages/coase%27s-penguin,-or,-linux-and-the-nature-of-the-firm/.

——— (2016) “Peer production and cooperation”, in J. Bauer and M. Latzer (eds.) Handbook on the Economics of the Internet. Cheltenham, UK and Northampton, MA: Edward Elgar Publishing.

Benkler, Y., A. Shaw and B. M. Hill (2015) “Peer Production: A Form of Collective Intelligence”, in T. W. Malone and M. Bernstein (eds.) Handbook of Collective Intelligence. Cambridge, Massachusetts: The MIT Press, p. 232. Available at: http://cci.mit.edu/Cichapterlinks.html.

Bianchini, M. and S. Maffei (2012) “Could design leadership be personal? Forecasting new forms of ‘Indie Capitalism’”. Design Management Journal 7(1): 6–17.

Bianchini, M., M. Menichinelli, S. Maffei, F. Bombardi and A. Carosi (2015) Makers’ Inquiry. Un’indagine socioeconomica sui makers italiani e su Make in Italy. Milano: Libraccio Editore. Available at: http://makersinquiry.org/.

Busacca, M. (2015) Lavoro totale: Il precariato cognitivo nell’era dell’auto-imprenditorialità e della Social Innovation. Doppiozero. Available at: https://archive.org/details/BusaccaLavoroTotaleCheFare.

Cantiere per pratiche non-affermative (2013) Designers’ Inquiry. An inquiry on the socio-economic condition of designers in Italy. Available at: http://www.pratichenonaffermative.net/inquiry/en/.

CBA. (2012) “The Fab Charter”. Available at: http://fab.cba.mit.edu/about/charter/ (accessed on 15 September 2014).

Cnel and Istat (2014) Rapporto Bes 2014: il benessere equo e sostenibile in italia. Roma: Istat. Available at: http://www.istat.it/it/archivio/126613.

Corbet, J., G. Kroah-Hartman and A. McPherson (2015) Linux Kernel Development. How Fast is it Going, Who is Doing It, What Are They Doing and Who is Sponsoring the Work. Linux Foundation. Available at: http://www.linuxfoundation.org/publications/linux-foundation/who-writes-linux-2015.

Design (2015) Available at: http://www.merriam-webster.com/dictionary/design (accessed on 31 December 2015).

Dougherty, D. (2005) “Welcome”. Make Magazine 1: 7.

Fondazione Nord Est and Prometeia (2015) Make in Italy. Il 1° rapporto sull’impatto delle tecnologie digitali nel sistema manifatturiero italiano. Roma: Fondazione Make in Italy CDB, ItaliaLavoro, Hewlett Packard, BNL Gruppo Bnp Paribas. Available at: http://www.makeinitaly.foundation/wp-content/uploads/2015/10/make_in_italy_rapporto_completo_impatto_tecnologie_digitali_nel_sistema_manifatturiero_italiano.pdf.

Gershenfeld, N. (2005) FAB: The Coming Revolution on Your Desktop – From Personal Computers to Personal Fabrication. New York: Basic Books.

Goetz, T. (2003) “Open Source Everywhere”. Wired 11(11). Available at: http://www.wired.com/wired/archive/11.11/opensource.html.

Hatch, M. (2014) The maker movement manifesto. Rules for innovation in the new world of crafters, hackers, and tinkerers. New York: McGraw-Hill Education.

Huffington Post (2013) “Crolla il popolo delle partite Iva: -400mila dal 2008”. 11 September. Available at: http://www.huffingtonpost.it/2013/11/09/partita-iva-crollo-lavoratori-autonomi_n_4245051.html.

ISTAT (2015) Annuario statistico italiano 2015. Roma: Istituto nazionale di statistica. Available at: http://www.istat.it/it/archivio/171864.

LimeSurvey Project Team and C. Schmitz (2015) LimeSurvey: An Open Source survey tool. Germany: LimeSurvey Project Hamburg. Available at: http://www.limesurvey.org.

McRobbie, A. (2015) “Is passionate work a neoliberal delusion?” Available at: https://www.opendemocracy.net/transformation/angela-mcrobbie/is-passionate-work-neoliberal-delusion.

——— (2016) Be Creative: Making a Living in the New Culture Industries. 1st edition. Cambridge, UK and Malden, MA: Polity.

Menichinelli, M. (2016) “Mapping the structure of the global maker laboratories community through Twitter connections”, in C. Levallois, M. Marchand, T. Mata and A. Panisson (eds.) Twitter for Research Handbook 2015 – 2016. Lyon: EMLYON Press, Pp. 47-62. Available at: http://dx.doi.org/10.5281/zenodo.44882.

Menichinelli, M., M. Bianchini, A. Carosi and S. Maffei (2015) “Designing and Making: What Could Change in Design Schools. A first Systemic Overview of Makers in Italy and Their Educational Contexts”, in A. Meroni, L. Galluzzo and L. Collina (eds.) The Virtuous Circle – Cumulus Conference – Milan, June 2015. Milan: McGraw-Hill Education Italy. Available at: http://cumulusmilan2015.org/proceedings/articles/abs-101-Training/.

Menichinelli, M. and A. Ranellucci (2015) Censimento dei Laboratori di Fabbricazione Digitale in Italia 2014. Roma: Fondazione Make in Italy CDB. Available at: http://www.makeinitaly.foundation/wp-content/uploads/2015/02/Censimento_Make_in_Italy.pdf.

Quinto Stato (2014) “I nuovi poveri sono gli autonomi a partita Iva”. Available at: http://ilmanifesto.info/storia/i-nuovi-poveri-sono-gli-autonomi-a-partita-iva/.

Raasch, C., C. Herstatt and K. Balka (2009) “On the open design of tangible goods”. R&D Management 39(4): 382–393. Available at: https://doi.org/10.1111/j.1467-9310.2009.00567.x.

Shirky, C. (2007) “Re: [decentralization] Generalizing Peer Production into the Physical World”. Yahoo! Groups. Forum. Available at: https://groups.yahoo.com.

Siefkes, C. (2008) From Exchange to Contributions: Generalizing Peer Production into the Physical World. Version 1.01b. Berlin: Siefkes-Verlag. Available at: http://peerconomy.org/text/peer-economy.pdf.

Teichgraber, M. (2016) “Labour market and Labour force survey (LFS) statistics – Statistics Explained”. Available at: http://ec.europa.eu/eurostat/statistics-explained/index.php/Labour_market_and_Labour_force_survey_(LFS)_statistics (accessed on 8 August 2016).

The Blueprint (2014) “An interview with Dale Dougherty”. 13 May. Available at: https://theblueprint.com/stories/dale-dougherty/ (accessed on 26 August 2015).

Thompson, C. (2008) “Build it. share it. profit. Can open source hardware work”. Wired Magazine 16. Available at: http://www.wired.com/techbiz/startups/magazine/16-11/ff_openmanufacturing.

Toombs, A., S. Bardzell and J. Bardzell (2014) “Becoming Makers: Hackerspace Member Habits, Values, and Identities”. Journal of Peer Production 5. Available at: http://peerproduction.net/issues/issue-5-shared-machine-shops/peer-reviewed-articles/becoming-makers-hackerspace-member-habits-values-and-identities/.

Troxler, P. (2011) “Libraries of the peer production era”, in Open Design Now: Why design cannot remain exclusive. Amsterdam: BIS Publishers. Available at: http://opendesignnow.org/.

von Hippel, E., J. D. Jong and S. Flowers (2010) “Comparing Business and Household Sector Innovation in Consumer Products: Findings from a Representative Study in the UK”. SSRN eLibrary. Available at: http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1683503.

von Hippel, E., S. Ogawa and P. J. de Jong (2011) “The age of the consumer-innovator”. MIT Sloan Management Review 53(1). Available at: http://evhippel.files.wordpress.com/2013/08/smr-art-as-pub.pdf.

Wolf, P., P. Troxler, P.-Y. Kocher, J. Harboe and U. Gaudenz (2014) “Sharing is Sparing: Open Knowledge Sharing in Fab Labs”. Journal of Peer Production 5. Available at: http://peerproduction.net/issues/issue-5-shared-machine-shops/.

Massimo Menichinelli, Aalto University & Fondazione Make in Italy CDB & IAAC | Fab City Research Laboratory

Massimo Bianchini, Politecnico di Milano, Dipartimento di Design

Alessandra Carosi, Politecnico di Milano, Dipartimento di Design

Stefano Maffei, Politecnico di Milano, Dipartimento di Design